Memo #12

Sound mind and a fool

The portfolio experienced volatility in Q4 25 after two core positions were established.

This memo serves to lay out the theses for these two positions briefly.

Vow ASA

Background

Vow ASA is a Norwegian cleantech technology company specialising in wastewater purification and waste valorisation solutions for the maritime and industrial sectors. Listed on the Oslo Stock Exchange since its 2020 rebranding from Scanship Holding ASA, Vow has positioned itself as a market leader in cruise ship environmental solutions while expanding aggressively into land-based industrial applications. Scanship (the maritime division) currently holds 40% market share and is rapidly rising.

Vow provides solutions addressing three overlapping global trends: maritime decarbonization (cruise ship environmental compliance), industrial waste valorisation (conversion of biomass and plastic waste into biochar and renewable energy), and circular economy transformation. The company operates in markets characterised by increasing regulatory pressure for environmental compliance and strong demand from industry players pursuing decarbonization targets. Its technology suite includes Scanship's wastewater and waste treatment systems (proven across multiple cruise operators), C.H. Evensen's large-scale pyrolysis furnaces (serving metallurgical and advanced materials industries), and ETIA's Biogreen pyrolysis process.

The set-up

The company has navigated significant operational and financial challenges over the past two years— including substantial cost overruns on industrial projects, profitability pressures, and debt covenant constraints—while simultaneously capitalising on strong demand from cruise industry fleet renewal. The company achieved a pivotal NOK 1 billion annual revenue milestone in 2024 and is undergoing strategic restructuring under newly appointed CEO Gunnar Pedersen, with a focus on restoring profitability and operational efficiency.

Its previous management team enjoyed high valuations and capital flows at the peak of the ESG cycle.

In August 2019, Vow (then Scanship Holding ASA) identified a strategic opportunity to expand beyond its core maritime wastewater purification business into broader industrial decarbonization. The acquisition of ETIA Ecotechnologies—a French-based developer of Biogreen pyrolysis technology—represented the company's first major foray into land-based circular economy solutions. The idea was to increase its Total Addressable Market share by targeting the global industrial decarbonization market, since it is much larger than its cruise ship environmental systems market.

Vow bought ETIA for NOK 180 million and C.H. Evensen for NOK 50 million. Vow deployed more than NOK 500 million, accounting for cumulative R&D and infrastructure investments spend.

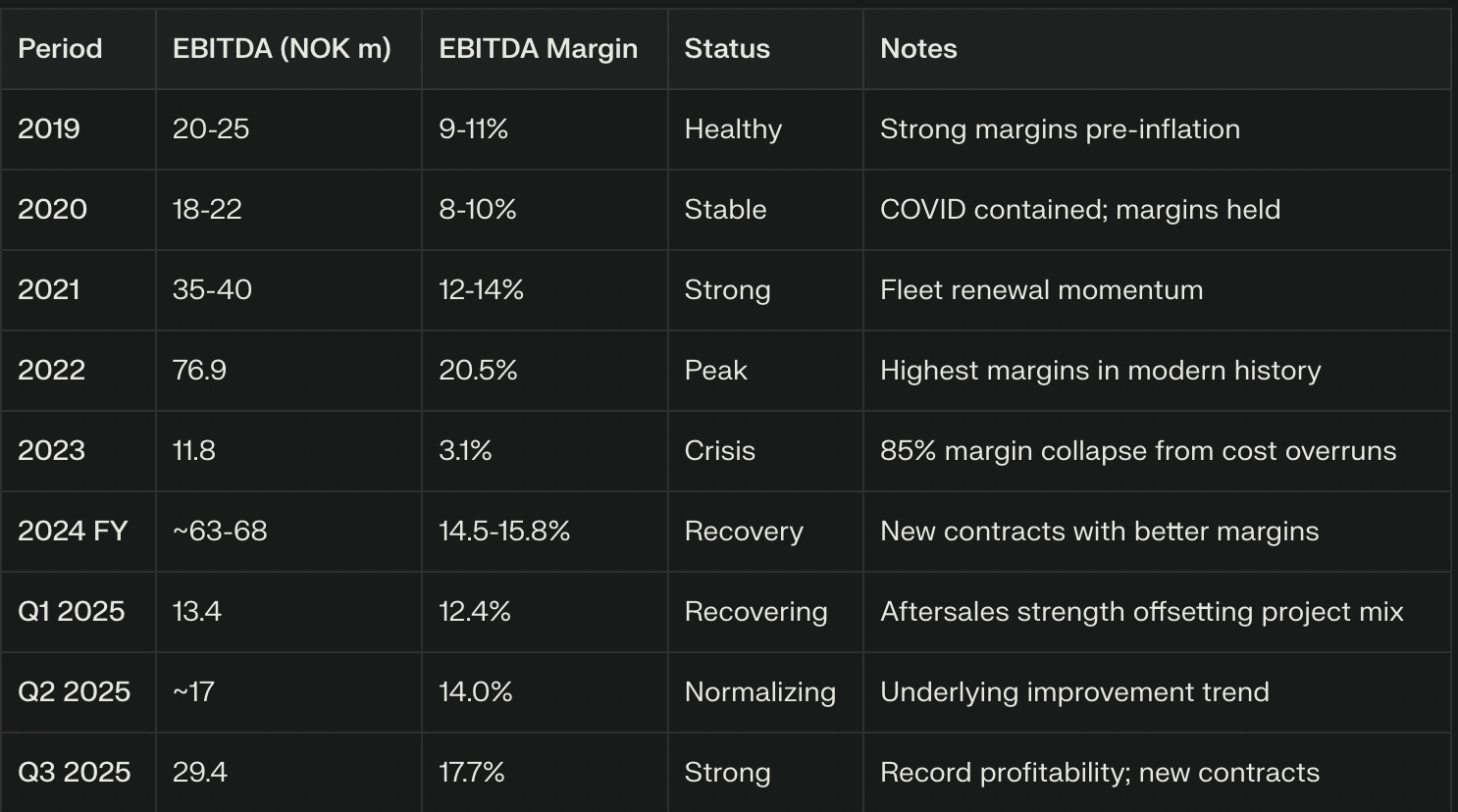

Since then, Vow struggled with developing and commercialising the technology in the market. Significant cost overruns reported in 2025 Q2 and Q3 led to write-downs and material losses. These projects were pivotal in proving its scalability. The industrial division has been disastrous.

Even as the maritime division continues to perform well and remains highly cash flow generative, industrials continue to be a cash sink. Vow’s profitability completely collapsed in 2023 as the supply chain costs escalated dramatically. Interest expenses ramped up as Vow had to finance its facility expansion.

Vow was heading for covenant breach in 2024 on its NOK 575M debt facility with DNB Bank ASA. The management negotiated a restructuring package comprising:

(1) a NOK 250 million fully underwritten rights issue—double the initially planned NOK 125 million minimum—at NOK 1.50 per share, raising gross proceeds through 166.7 million new shares plus 9.9 million underwriting commission shares;

(2) amended debt covenants, including relaxation of Debt Service Cover Ratio (DSCR) to 1.0x through year-end 2025, Equity Ratio minimum of 20.0% through maturity, and suspension of NIBD/EBITDA ratio requirements;

(3) a NOK 125 million liquidity bridge facility from DNB to fund operations pending rights issue completion; and

(4) a 12-month extension of loan facility maturity to Q3 2027. The restructuring was completed by December 2024, providing critical financial breathing room while diluting existing shareholders by approximately 60% and positioning DNB as the company's largest shareholder (25.67% post-transaction).

The suspension of the leverage ratio covenant provided Vow with much-needed breathing room to focus on execution, free cash flow generation, and the optimisation of its assets.

In summary, we have Vow holding both the crown jewel, Scanship, and a disastrous Industrial division. Shareholders are also exhausted by the perennial bombardment of bad news from Industrials, and the 60% equity dilution in 2024 to avoid bankruptcy was the nail in the coffin.

The new management team

The new management team replaced the old in May 2025, removing Henrik Badin, whose team is largely responsible for the dirt Vow has to dig out of, with CEO Gunnar Pedersen. Gunnar was previously an executive VP in Kongsberg Maritime, a subsidiary of a NOK $294 billion market capitalisation company.

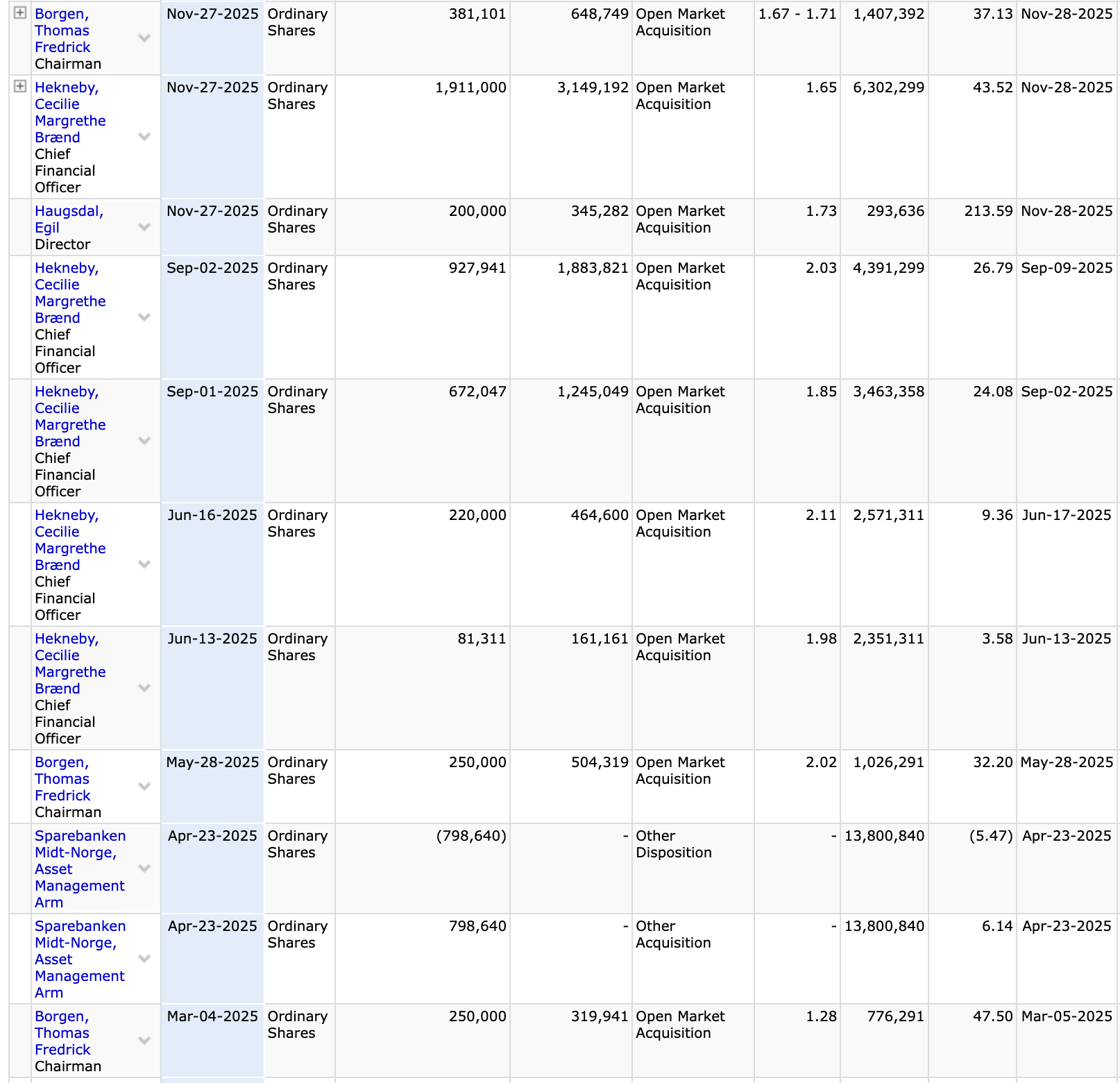

CFO Cecilie Hekneby was the CFO of Spir Gorup ASA, a NOK $5 billion company acquired in September 2023. The company received an offer 66.7% above the market price before the announcement. Cecilie and her family have a history of purchasing shares using their own wealth, aligning themselves strongly with shareholders.

Here, we observe a consistent and aggressive accumulation of shares by insiders since May 2025. Since then, they have tidied up and continue to address accounting and operational issues left by the previous management team. They successfully negotiated twice with their debtor to waive the covenant trips. They have much better contract terms for Vow with increased average contract value, profitability, flexibility, and working capital timings.

Even as they openly communicate the difficulties they face, the strategy they are employing, and the bumps along the way, they have only dialled up their share purchases.

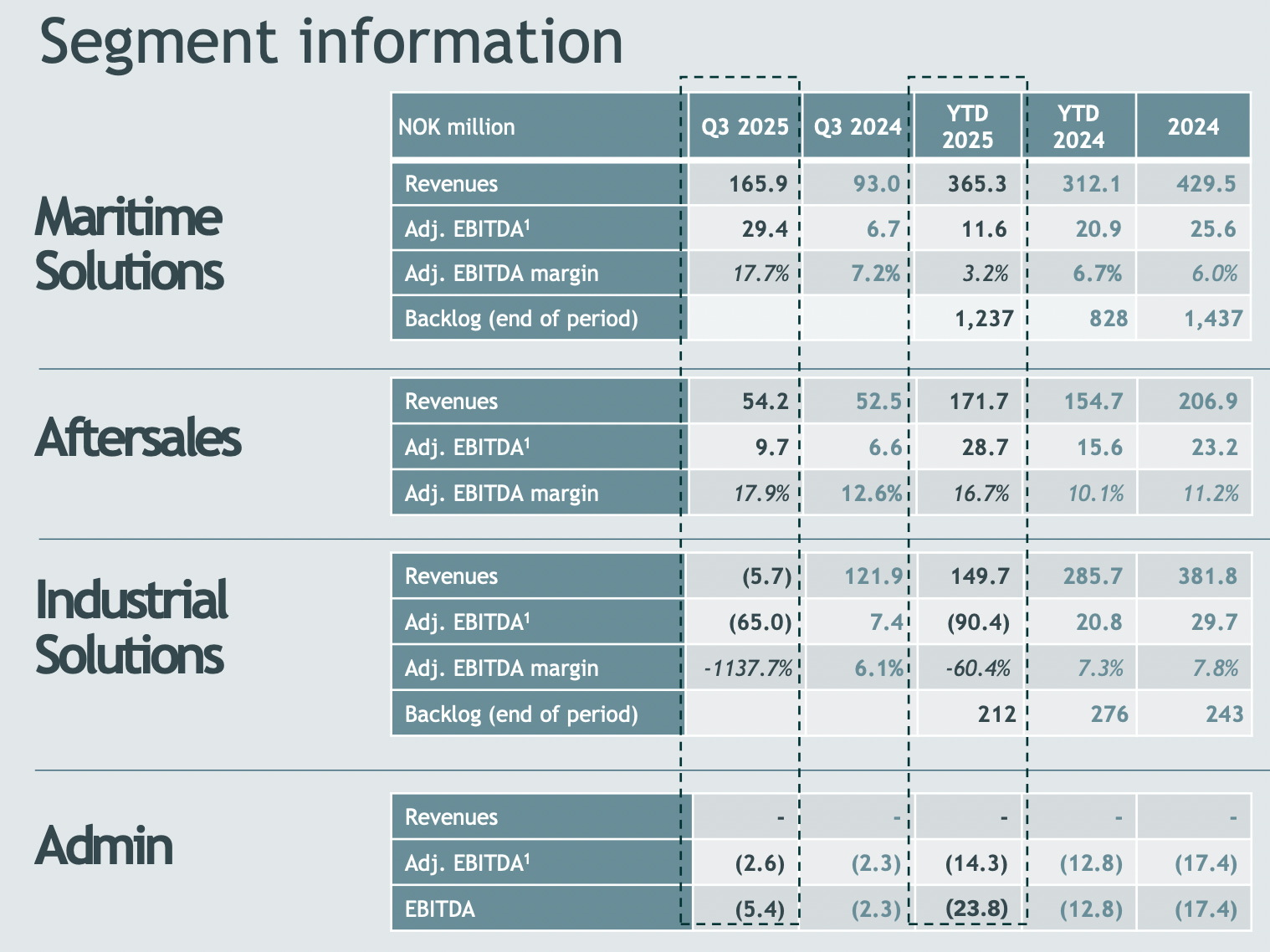

Scanship (Maritime)

Scanship has emerged as the market leader in cruise ship wastewater purification and waste valorisation, commanding approximately 40% of the global market share and 71% of the addressable 2024-2028 cruise newbuild market.

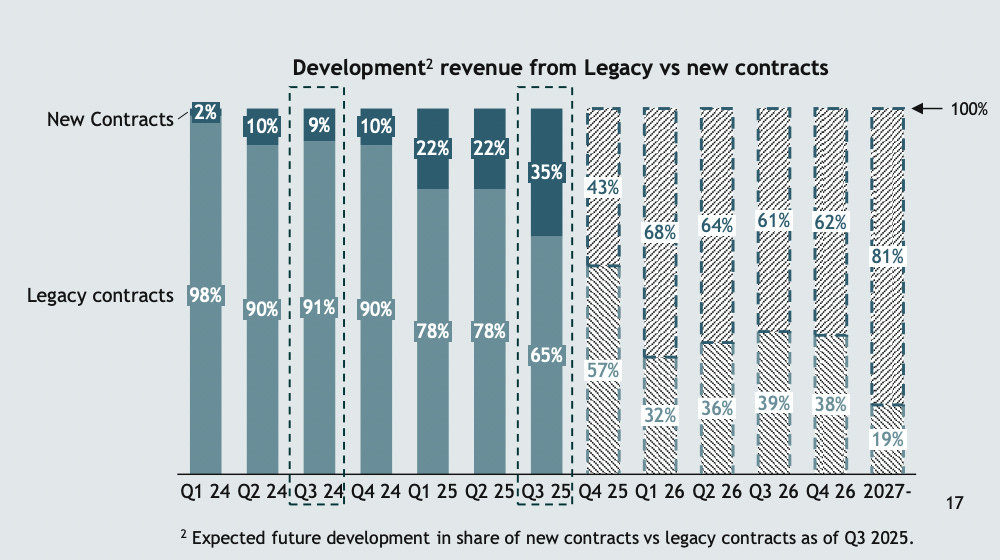

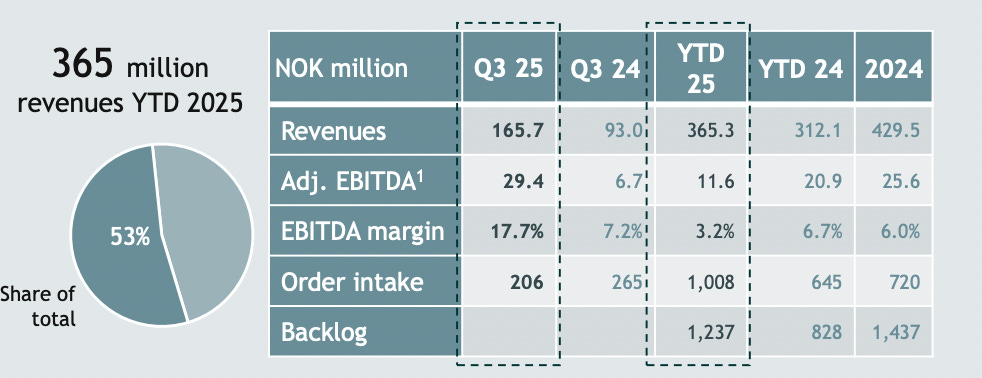

Over the past five years (2019-2025), Maritime Solutions almost doubled its revenue—from NOK 221 million in 2019 to NOK 430 million in 2024. During this period, the division transformed its contract economics, moving from unprofitable legacy contracts (0-8% EBITDA margins) to high-quality new agreements (>20% EBITDA margins). The division’s order backlog has expanded from NOK 584 million at the end of 2022 to NOK 1,449 million in Q3 2025, providing 12-14 months of revenue visibility with contracted deliveries extending through 2032-2033.

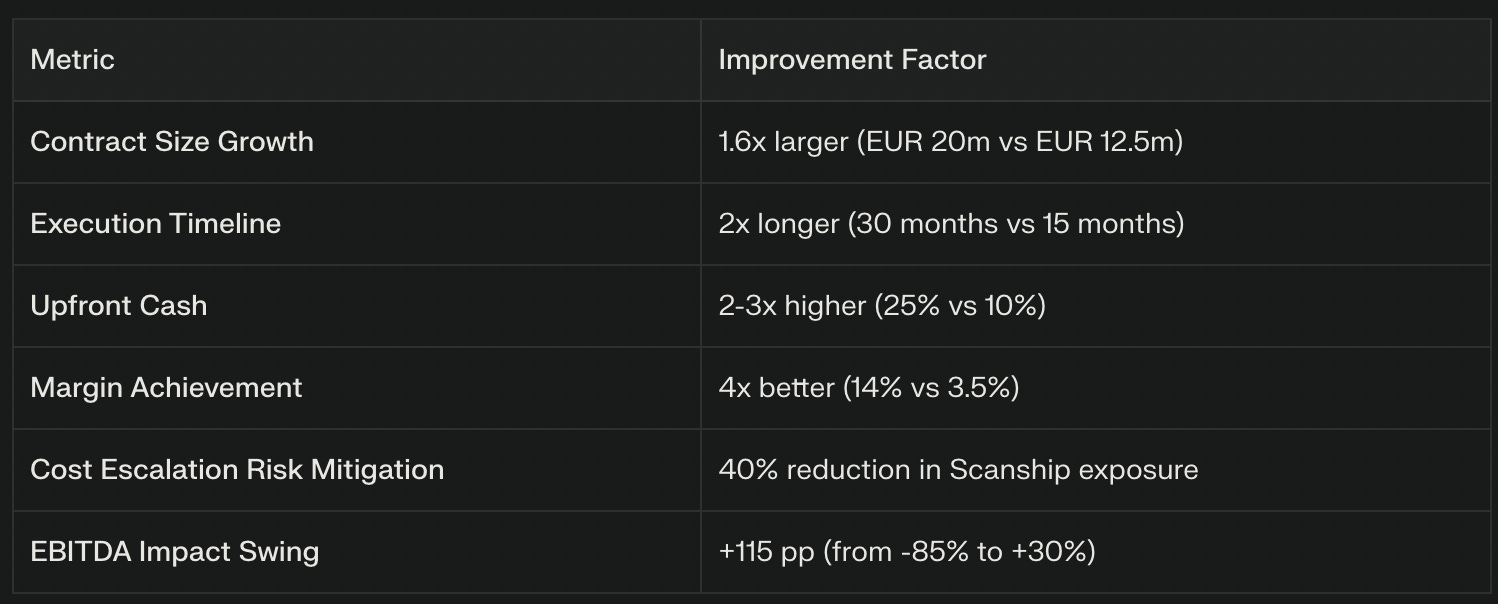

The new management has implemented two critical changes in the new contracts:

Improved Contract Pricing Discipline: New contracts signed in 2024-2025 include cost escalation clauses (labour, materials, freight), enabling Scanship to pass through inflationary impacts rather than absorb them.

Longer Delivery Timelines: New contracts feature 2-3 year delivery windows (vs. 12-18 months historically), reducing execution risk and allowing better resource planning.

The result is that Q3 2025 EBITDA margin reached 17.7%—the strongest in recent history—as the backlog transitioned from executing legacy low-margin contracts to deploying new high-margin contracts.

Scanship stands to receive much greater benefits from these new contracts over the next two years as the legacy contracts phase out organically.

Scanship enjoys a high retention rate because of its niche. The risk of switching to a less reputable newcomer will be too much risk to bear for too little cost savings. This explains its minimal churn inferred by its repeated contract wins.

A mid-size ship of 1,000 to 2,500 passengers costs around $600 million; large ships with more than 5,000 passengers cost more than $1.2 billion. With the average contract value of around USD $24 million, it represents less than 2.5% of the total construction cost. Track record and reputation matter much more than any minute cost savings. Why risk a $1 billion ship for a $5 million saving?

The Aftersales division provides recurring spare parts and consumables for an installed base of 183+ Scanship-equipped cruise ships. In 2024, it generated NOK 208 million in annual revenues and contributed 14-17% in EBITDA margins. Beyond profitability, Aftersales delivers operational stability and strengthens customer relationships that drive new contract wins.

Considering how its backlog has been growing with rapidly improving industry dynamics and the new management’s strong track record in execution thus far, maritime revenue is expected to double over the next two to three years and perhaps grow at mid-teens thereafter.

In 2027, the maritime division is expected to generate NOK $1 billion, with 25% EBITDA margins. Expected 2027 EBITDA: NOK $250 million. It is difficult to identify direct competitors given Scanship’s dominance. 71% market share over 2025-2027 newbuilds. Incumbents can easily be valued at 2.0x of the other players because of their bargaining position. Alfa Laval 15.0x EV/EBITDA, Kongsberg 27x, and Wartsila at 14.0x.

At a mere 10.0x multiple, Scanship is valued at NOK $2.5 billion. At 15.0x, $3.75 billion.

The aftersales division grows proportionally with the installed fleet. With Scanship’s market share increasing by 75% from 40% to 71%, we expect the aftersales division’s revenue to rise accordingly by 2027. Aftersales margins have improved from 12.6% in Q3 2024 to 17.9% in Q3 2025. This is expected to increase further to the mid-20s by 2027. At $350 million in revenue and 25% EBITDA margins, we expect $87.5 million in EBITDA. At 10.0x EV/EBITDA, that is NOK $875 million.

Adding both together gives us NOK $4.65 billion. Subtracting the net debt of NOK $523 million gives an implied equity value of $4.13 billion (+460% upside).

Vow’s current market capitalisation stands at NOK $737 million. This disconnect reflects a few possible reasons: (1) the industrial segment is a huge cash drag and masks the profitability and strength of the maritime division; (2) scepticism in execution; (3) underappreciating the fundamental improvements that have already taken place; (4) underappreciating the quiet and strong alignment of insiders; (5) covenant concerns; (6) debtholder selling out as equityholder.

What are the different ways Vow can close this gap?

(1) Continue executing as they already do

(2) Shrewd capital allocation - deleverage then buyback shares if valuation remains disconnected

(3) Sell off the industrial division, highlight true shareholder value.

Since Q3 25

2 major contract wins worth EUR 43.4 million = NOK $505 million in Nov/ Dec 25.

Large shareholder DNB Bank (debt converted) sold half of its stake at NOK 2.40 a share, leading to the share price falling from NOK $3.50 to $2.60. The market remains depressed in anticipation of further share dumping. Insiders took this opportunity to add more shares. DNB was never in the business of owning shares; they became shareholders as part of the restructuring deal. We have also added at this level.

Conclusion

We have a company with a long and complicated history under the poor stewardship of the previous management. The new management took over, bought shares with their personal wealth, communicated problems transparently, provided clear evidence of execution so far, and has been managing debtholders well.

At $737 million market capitalisation, $160 million spot EBITDA, ignoring industrials, ignoring future fundamentals improvements.

European Lithium (EUR.AX)

Please refer to my memo #11 for a recap of the thesis. But honestly, the reason why EUR.AX is my core position is because of God. I have reservations about certain behaviour and the thesis itself, but I am choosing His way rather than my own understanding here.

Anyway, the thesis is still playing out, albeit with huge volatility, which affected our 2025 performance. I added more to my position at $0.15 AUD.

Since the last report, the main developments are:

Offtake agreements confirmed with Saudi JV and Romania

CRML released more drilling numbers

CEO commented on the new airport for logistics

EUR bought back some shares

Trump is going after Greenland and is talking about REE again

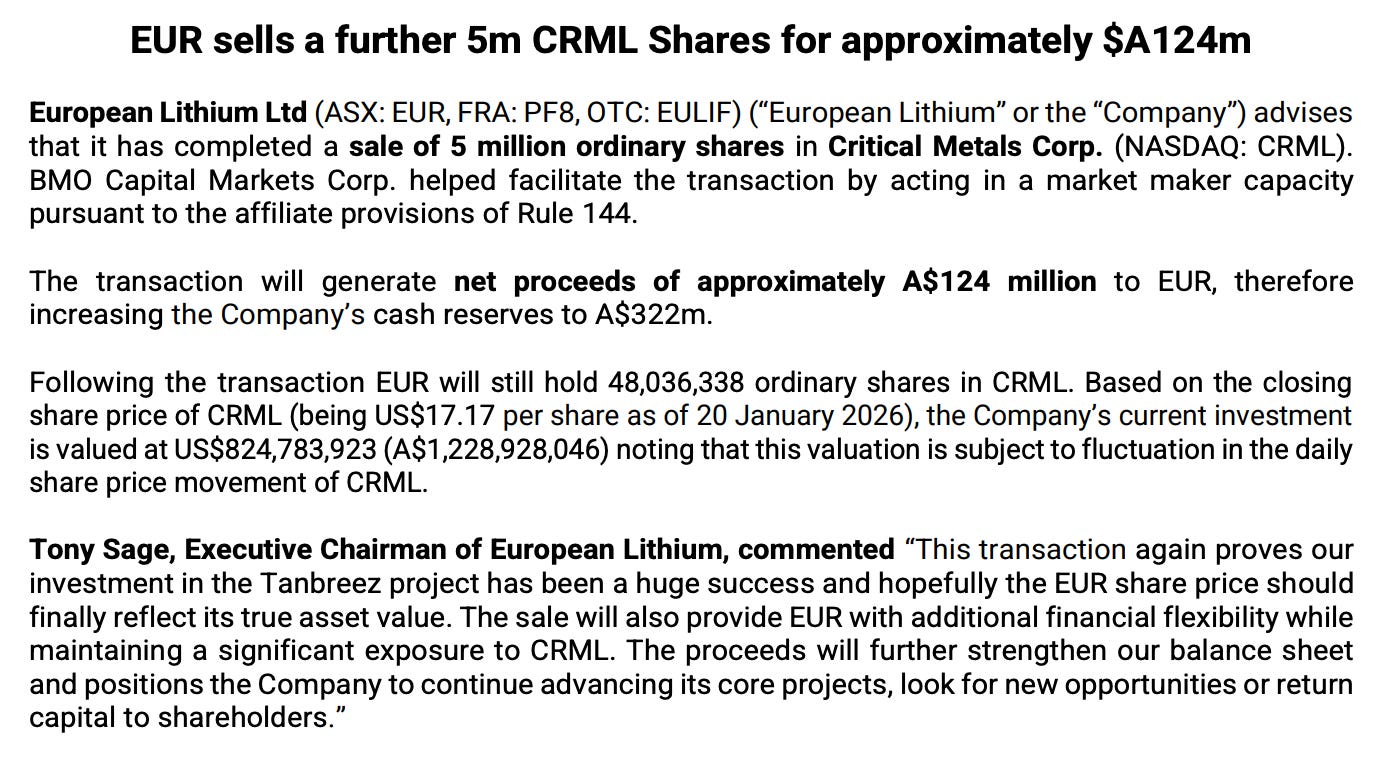

EUR sold 5 million more CRML shares at USD $16.9 per share

Current net asset value of EUR stands at A$322m (cash) + A$1,228,928,046 (CRML stake) + 7.5% Tanbreez stake + other holdings in the public market

NAV per share: A$0.75 (>100% upside)

Current share price: A$0.30

Thank you for reading.

God bless,

Joshua

For if we are beside ourselves, it is for God; or if we are of sound mind, it is for you.

2 Cor 5:13

Disclaimer:

The information contained herein reflects the opinions and projections of Joshua Zeng, as of the date of publication, which is subject to change without notice at any time after the date of issue. All information provided is for informational purposes only and should not be deemed as investment advice or recommendation to purchase or sell any specific security/asset. While the information presented herein is believed to be reliable, no representation or warranty is made concerning the accuracy of any data presented. Positions reflected in this presentation do not represent all the positions held, purchased, or sold, and in the aggregate, the information may represent a small percentage of activity. The information presented is intended for Joshua Zeng to illustrate his own thoughts for his own learning purposes only. All funds managed under Joshua Zeng wholly belong to him and him alone.

Please note that I frequently enter and exit portfolio positions quickly. I exit positions when there are superior ideas, when I realise I am wrong, or when the thesis has played out. Please do your own due diligence.