Memo #11

Portfolio Updates

Over the next few memos, I will provide brief updates on the core positions in the portfolio. The portfolio is currently 66% invested. I will continue to search for new ideas as led by God.

European Lithium Ltd. (EUR.AX/ EULIF)

European Lithium is an ASX-listed Lithium mining exploration company focused on a project in Austria. It also has a collection of assets and equity stubs in other projects under other listed companies.

Equity stakes in developers:

a. 10% of Cyclone Metals Ltd (ASX:CLE). CLE signed an agreement with VALE SA to develop the Iron Bear Project. Worth $7MM AUD.

b. 12% in CUFE Ltd (ASX: CUF). Copper/gold project in Tenant Creek. Worth $2MM AUD.

c. 16% in Moab Minerals Ltd, holds Uranium exploration projects in Tanzania.

EUR owns 56MM shares (~50%) of CRML, Critical Metals Corp. Critical Metals Corp’s flagship project, Tanbreez, is one of the world’s largest, rare-earth deposits located in Greenland. CRML has a 92.5% stake in Tanbreez, while EUR owns the remaining 7.5%.

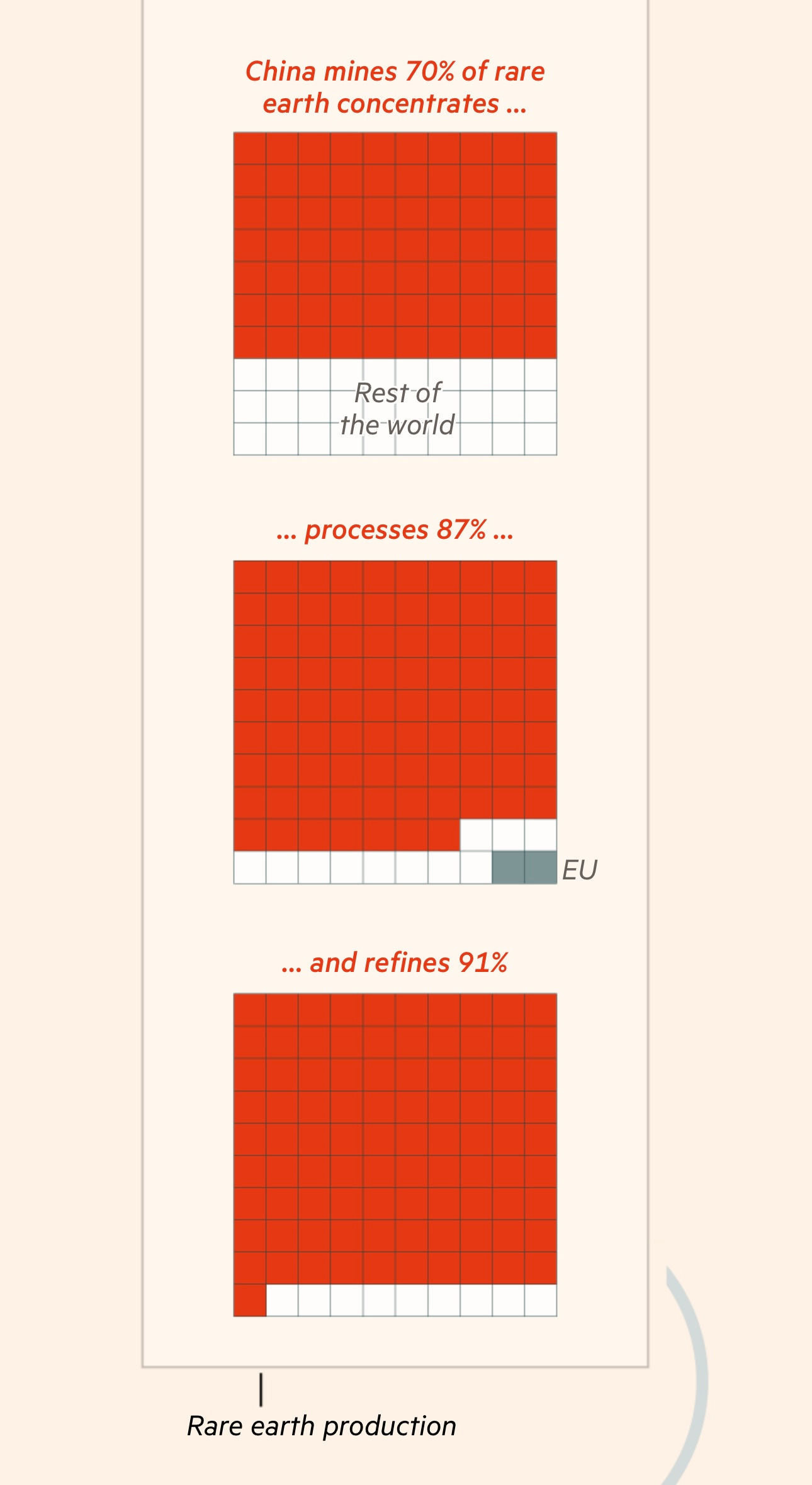

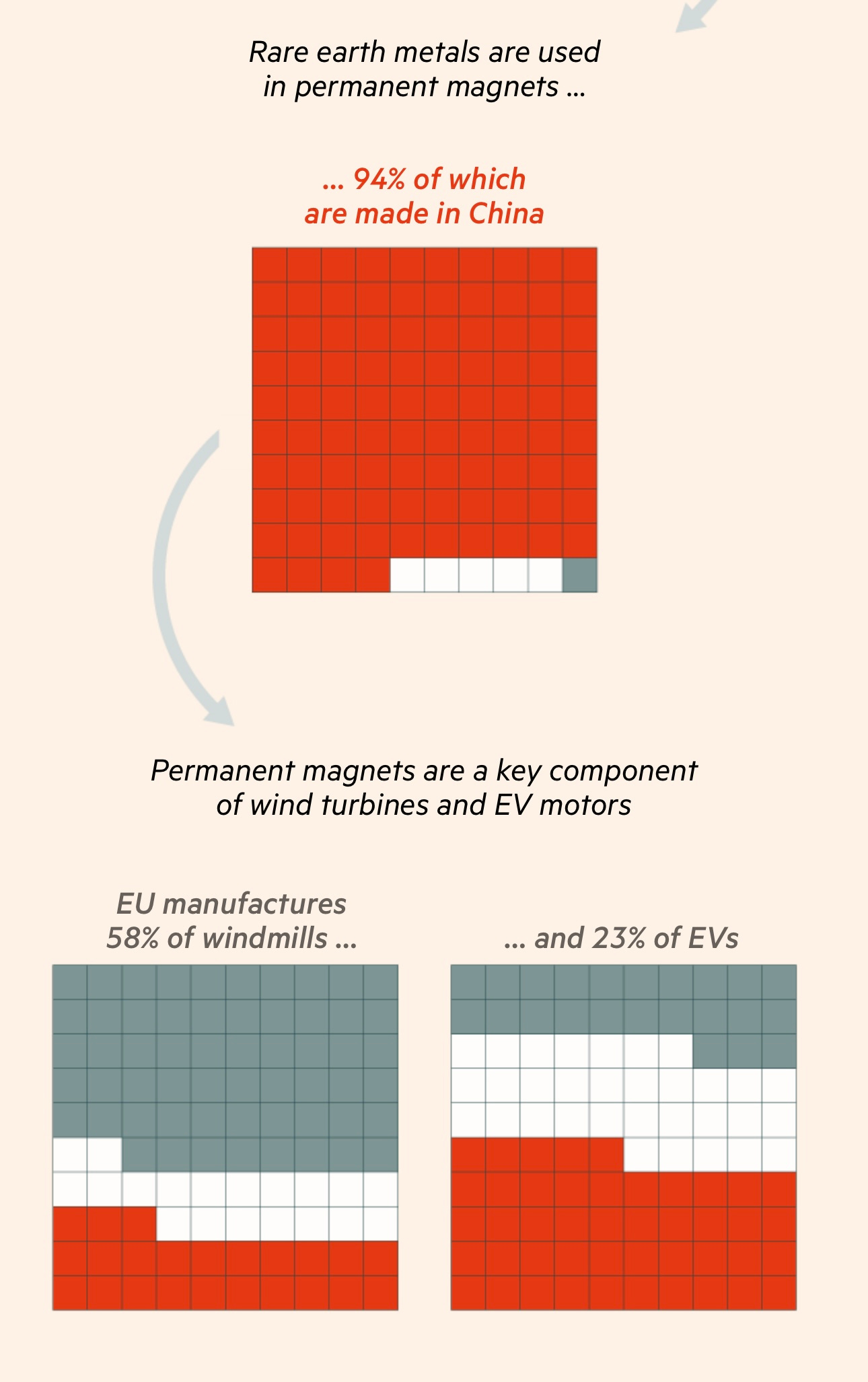

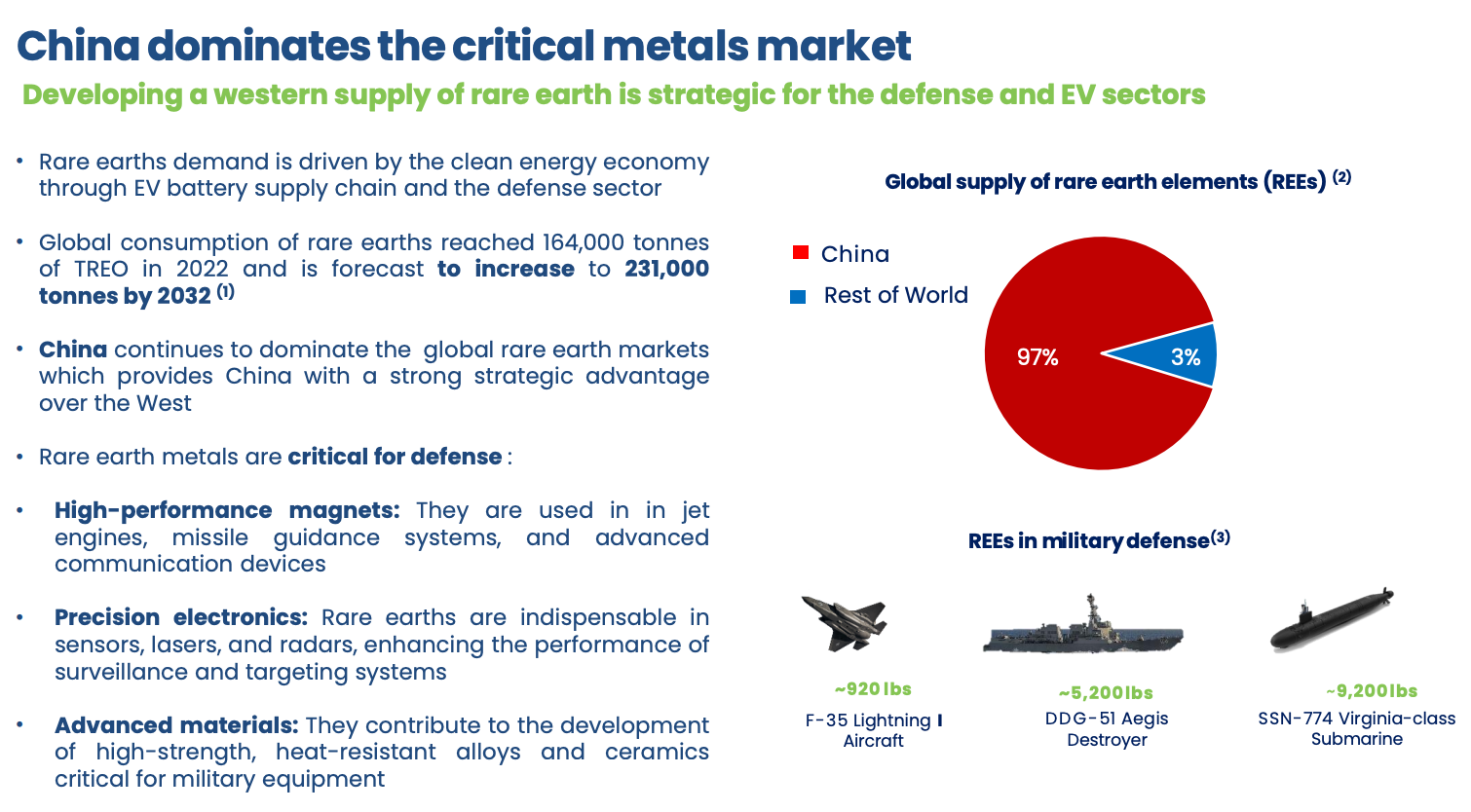

The Rare Earth Element (REE) industry has quickly become a fierce and contentious battleground between the West and China. REE is used in permanent magnets, catalysts, metallurgy, battery alloys, and many more. They are essential in the production of hybrid and electric vehicle engines, generators in wind turbines, hard disks, cell phones, and defence systems.

However, China controls most of the supply chain, capable of holding the rest of the world hostage. The following infographics from FT and Critical Metals Corp summarise this nicely.

Hence, the West, led by President Trump, has been scrambling to secure REE assets all over the world.

In February 2021, President Biden signed an executive order to secure the domestic supply chain for REE. Bipartisan legislation was introduced in the U.S. Senate in January 22 to force defense contractors to stop buying rare earths from China by 2026.

On 10 July 25, MP Materials entered into a partnership with the US Department of Defense to ‘dramatically accelerate the build-out of an end-to-end U.S. rare earth magnet supply chain and reduce foreign dependency.’

DoD has entered into a 10-year agreement establishing a price floor commitment of $110/kg of NdPr products stockpiled or sold, and has received cheap financing from the market. DoD has also purchased $400M of MP Materials convertibles.

Since then, the U.S. government has struck numerous deals with companies in industries it categorised as critical.

China retaliated by flexing its muscles and starting the timer for the West to secure its own supply of REE.

The Pentagon is going on a $1B Critical Mineral buying spree.

However, I am neither an REE expert nor a trader who knows how to trade around momentum. While the industry recovery seems to be in the early innings of the current cycle, I do not have any edge over the typical REE investor in the market.

So why EUR?

As mentioned above, EUR owns 56MM shares of CRML and 7.5% of the Tanbreez project.

CRML is priced at $17 per share today in the market, $952MM USD = $1.46B AUD. If CRML is at $1.9B USD market cap and owns 92.5% of Tanbreez, it implies that EUR’s 7.5% stake of Tanbreez should be valued at 155M USD = 238M AUD.

Total value of CRML shares + Tanbreez = $1.7B AUD.

EUR is currently trading at less than 400M AUD, fully diluted market capitalisation, accounting for future dilution, and little share buybacks.

This huge discount will only close if the management is (1) incentivised to and (2) shrewd in capital allocation.

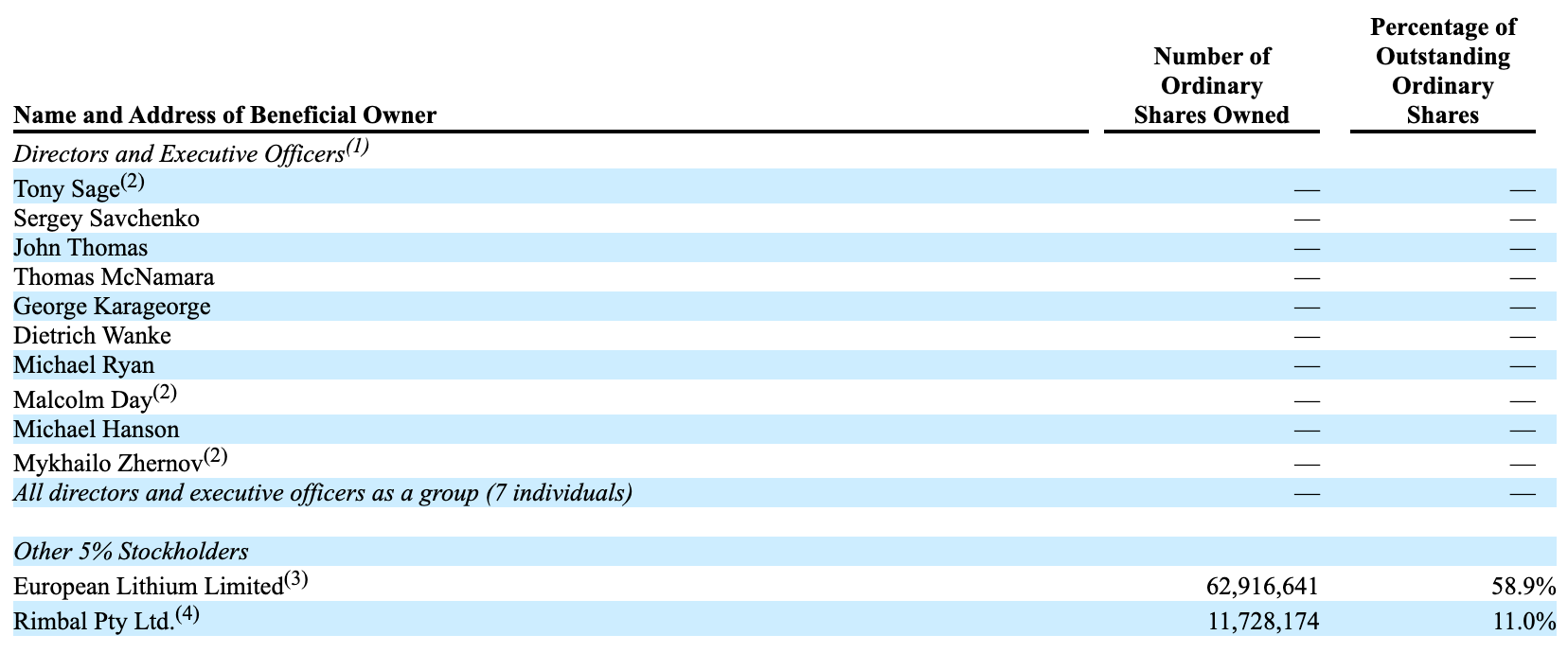

First, incentives. Let’s look at the insider ownership of CRML.

As of 30 Jun 25, it is reported in their 20F that the insiders own no shares directly, and most own CRML through their ownership of EUR. Of course, the management is issued RSU’s as part of their compensation and bonuses.

Total number of diluted shares outstanding: 2B (note: currently 1.35B, 2B considered the extreme case, a part only vests end Sep 26, not accounting for 10% share buyback 17 Oct onwards)

The directors of EUR and CRML, Antony Sage (~100M), Malcolm Day (~59M), Michael Carter (~22M), and Mykhailo Zhernov (~68M) are all notable shareholders of EUR, with their shareholding far outweighing their annual cash compensation.

The company has started to liquidate its CRML shares to raise cash in its balance sheet and intends to buy back its shares aggressively.

Current cash position on balance sheet: >$100MM AUD (accounting for sale of CRML shares since 30 June 25)

Value of CRML shares: $1.46B AUD

Implied value of 7.5% Tenbreez interest: $238MM AUD

Total value: $1.8B AUD

NAV per share: 0.90 AUD (+298%)

Average initiated cost price: 0.226 AUD

Implied diluted market cap: 452MM

Cash buffer on its balance sheet will increase over time as the company continues to crystallise the value of its CRML shares and buy back its own shares, hence further increasing its NAV per share.

Furthermore

Why the huge discount? What can go wrong?

EUR has diluted its shares substantially over the last year to get to this stage, causing huge concerns in the market regarding the possibility of further dilution. Given that the management team is now aligned, it makes perfect sense that they decide to buy back shares to increase the fair value per share.

CRML can also suddenly crash back to earth if REE security is no longer an issue or if offtake agreements fall apart. Perhaps if an unexpectedly huge supply of REE stockpiles and refining capacity surfaces somewhere in the West, or if all trade relations between China and the West are restored.

Until then, EUR continues to liquidate its CRML holdings, buy back its shares, and hold cash in its balance sheet.

Please note that this is a brief overview of EUR; there is much more beneath the surface to be understood.

God bless,

Joshua

Disclaimer:

The information contained herein reflects the opinions and projections of Joshua Zeng, as of the date of publication, which is subject to change without notice at any time after the date of issue. All information provided is for informational purposes only and should not be deemed as investment advice or recommendation to purchase or sell any specific security/asset. While the information presented herein is believed to be reliable, no representation or warranty is made concerning the accuracy of any data presented. Positions reflected in this presentation do not represent all the positions held, purchased, or sold, and in the aggregate, the information may represent a small percentage of activity. The information presented is intended for Joshua Zeng to illustrate his own thoughts for his own learning purposes only. All funds managed under Joshua Zeng wholly belong to him and him alone.

Please note that I frequently enter and exit portfolio positions quickly. I exit positions when there are superior ideas, when I realise I am wrong, or when the thesis has played out. Please do your own due diligence.