Memo #8

Refreshed framework and review

The portfolio is down around 10% YTD vs >22.6% YTD for the S&P 500. The underperformance is attributed to my poor decisions, an imperfect process, and a tinge of poor luck. This memo reflects my thoughts and how my faith has influenced my investment process since two months ago.

Just a heads up - I plan to be completely transparent and will not be mincing my words. The ease of doing so is a privilege gifted by God since I am mainly accountable to myself and Him.

Part A. Process

The Bottom Line

My process has always revolved around arbitraging market expectations (market price) and expected probabilistic reality (fair value). This has not changed. I firmly believe that true value is typically only created when an investor is rewarded for being contrarian and right about it.

A long-term-oriented compounder investor beats the market by being more right than the market about the prospects and invests at a less-than-fair price today. The fair value is a function of the probabilities of potential future developments. It accounts for the impacts of disruption, widening moat, capable management, key-man risks, expanding pricing power, or loss of bargaining power.

The wise investor understands the business prospects and identifies the key factors that make or break the thesis. The investor then evaluates what the market price is already pricing in. We have a poor ability to visualise the effects of compounding. 10% compounded for 50 years nets you 117x while 12% compound for 50 years gives you 289x. A measly 2% difference today can yield a much larger delta in the future.

Let’s consider a very simplistic example. Is 100x P/E considered expensive? As you’d have guessed, it depends on the quality of the business. If it is conservatively expected to compound at 50% per annum for the next 10 years, its earnings power will be 58x today’s. So in this case, at 100x P/E, while the market may already seem optically sanguine about its prospects, it is perhaps not nearly optimistic enough. One can argue that the market is myopic and falls for the age-old heuristic of failure to visualise and account for the effects of compounding.

I am not competitive enough to fish in the sea where other intelligent fishermen fish. To improve my chances of finding underappreciated businesses, I fish in neglected little ponds; where the mighty fishing trawlers operated by experienced and skilful fishermen cannot access. These are also unattractive to casual fishermen but beneath the murky waters are the Arowanas.

Acknowledgement for God

I spent considerably more time with God for the last few months, not as a religious activity but as an attempt to learn more about my creator. I was led on a journey by God to discover His nature, understand His sovereignty, and recognise my deficiencies. It is truly liberating to recognise that all the efforts, successes, and learning I have been gifted come from God rather than my efforts. I have always wondered what I have done to deserve such luck - to do what I am passionate about and for it to feed me for the rest of my life. I was right that I did not deserve it. I was wrong that I was just lucky.

It is by grace that He led me here, by grace that He taught me His ways, and by grace that He prepared the path for me through my investing journey. He did not show His love to me by providing me abundantly materially. He showed His love to me by granting me the ability to chase Him rather than mammon, to chase His wisdom rather than man’s wisdom.

It is a work-in-progress and the following is what He has led me to thus far.

A. The Foundation

I mentioned above that the bottom line remains to find inefficiencies in which market expectations differ from rational reality. The judgment behind what market expectations entail and what rational reality could be is paramount.

The remaining part of the memo attempts to flesh out the framework behind deriving these two numbers.

As you do not know the way the spirit comes to the bones in the womb of a woman with child, so you do not know the work of God who makes everything.

Ecclesiastes 11:5

It is pertinent to recognise that correct judgment relies on the quality of my thinking, the quality and quantity of information available, and the inherent ‘randomness’ of interactions. Improbable worst cases will happen, investment theses will fall apart, and some things inevitably go wrong. It is hubristic for a capital allocator to get excessively involved with any single position because he thinks he is right. Investing is more of an art and any final decision reflects the artist’s process and opinions. No one gets it right all the time.

More so than that, it is to have humility before God. To recognise that we don’t know it all and we aren’t God, and that is fine. We depend on Him and work within our limitations in reasoning, understanding, and knowledge.

B. The Obvious

… and if a tree falls to the south or to the north,

in the place where the tree falls, there it will lie.Ecclesiastes 11:3 (b)

Common sense is uncommon in an environment where emotions, heuristics, and incessant noise bombard the stock tickers. Even if the average trader has perfect information on prices in 5 years, he will likely trade his wealth away around that price target before then.

There are three parts to this:

Identify the overlooked opportunity (that is obvious)

Identify the non-fundamental reasons behind why it is overlooked

Know how to position for reversion to rationality

Let’s go back to first principles. You want to ace your final exams and have a choice between taking a primary 1-level paper or a university-level exam. Even if you are perhaps a professor in the relevant subject, would you pick the latter over the former? Perhaps for intellectual curiosity of sorts, sure. But if the only goal is to ace the exam, that is, to maximise your future expected returns over time, would it not make more common sense to solve easier puzzles than harder ones - if the rewards are the same?

Of course, it is not as simple. Hindrances typically stand in the way of the pursuit of the obvious. It is more impressive to solve difficult questions. Getting Amazon right is more remarkable than getting Gulf Marine Services right. The investor of the obvious may not have much to add to a conversation about AI, semiconductors, renewable energy, or potential rate cuts.

The obvious can be boring. The thesis may be relatively shorter in content with plenty of waiting. The obvious makes the investor feel dumb most of the time. The obvious may remain ignored as the market hits its 46th record high for the year.

There are reasons why seeking the obvious is not the obvious mandate for most investors. I, too, am guilty of ignoring the obvious because of distractions.

Let’s finally define what obvious is. It is not just having a good potential 'set-up’ where pieces seem to be in place. It is a clear inevitability because of today’s (and past’s) state but somehow overlooked. Better still, the company may already be generating the results today but masked by veils that will be removed.

C. Inflection

If the clouds are full of rain,

they empty themselves on the earth …Ecclesiastes 11:3 (a)

The market strives to be forward-looking and does a pretty good job. However, occasionally, market mood swings lead to confusion and volatility. The more efficient the market, the more likely the market is to price in reality rationally. The greater the number of eyes looking at the company, the more likely prices are already fair.

However, in the small pond, it is more common to find companies with prices that reflect the historical state (recency bias) and not the expected future outcomes. This coupled with inflecting events can lead to explosive market reactions.

There are three main types of inflections that I look out for:

Inflection of business fundamentals: On the brink of huge changes in business fundamentals that are already clearly taking shape or easy to achieve but not priced-in.

Inflection of capital structure: Recent painful restructuring may lead to shareholder fatigue that becomes an overhang over the stock price for a while. This occurs even though the restructuring might have drastically improved its financial health.

Inflection of profitability: Profitability might have been hidden by underperforming non-core operations, temporary mismanagement, changes in business fundamentals, or changes in industry dynamics. The market may completely discount the inevitable.

Of course, these three are largely intertwined and have compounding interactions that should not be underestimated.

D. Origins of opportunities

Understanding how opportunities come about helps to form a complete picture of the narrative that drives our thesis. The following list is not exhaustive and serves as examples that reflect the nature of the origins.

Nano and small-cap that are under- or uncovered by analysts. Investors typically seek validation from other smart analysts. The absence of recommendations and views may be psychologically too risky for most.

Institutional or major shareholder dumping. There are many reasons why one may sell and they can be non-fundamental. They could be selling or buying due to institutional imperative.

Some examples are:

Selling because the company was removed from the index

Selling because the company was delisted

Selling because it received a poor ‘ESG' rating

Selling because of their investors’ pressures

Selling because they received a small spun-off company in a different industry (no longer under ‘mandate’)

Selling because of personal biases

Selling because of personal incentives

Shareholder fatigue. Very often after the stock falls by 80-90%, the shareholder loses faith instinctively, without any regard for any potential change in fundamentals. The management might have been swapped out, the debt load might have been manageable now, and the underlying business may be strong today. But all these don’t matter because of exhaustion.

Illiquidity. Illiquidity is an accompaniment to the above. Price actions are more volatile. Illiquidity exacerbates the psychological biases behind the other factors.

However, more often than not, the reasons behind the fall are perfectly justified. Fundamentals might have deteriorated, the worst case might have happened, or something negative and unexpected impacted the company. It is my job to sieve out the gold from the gunk.

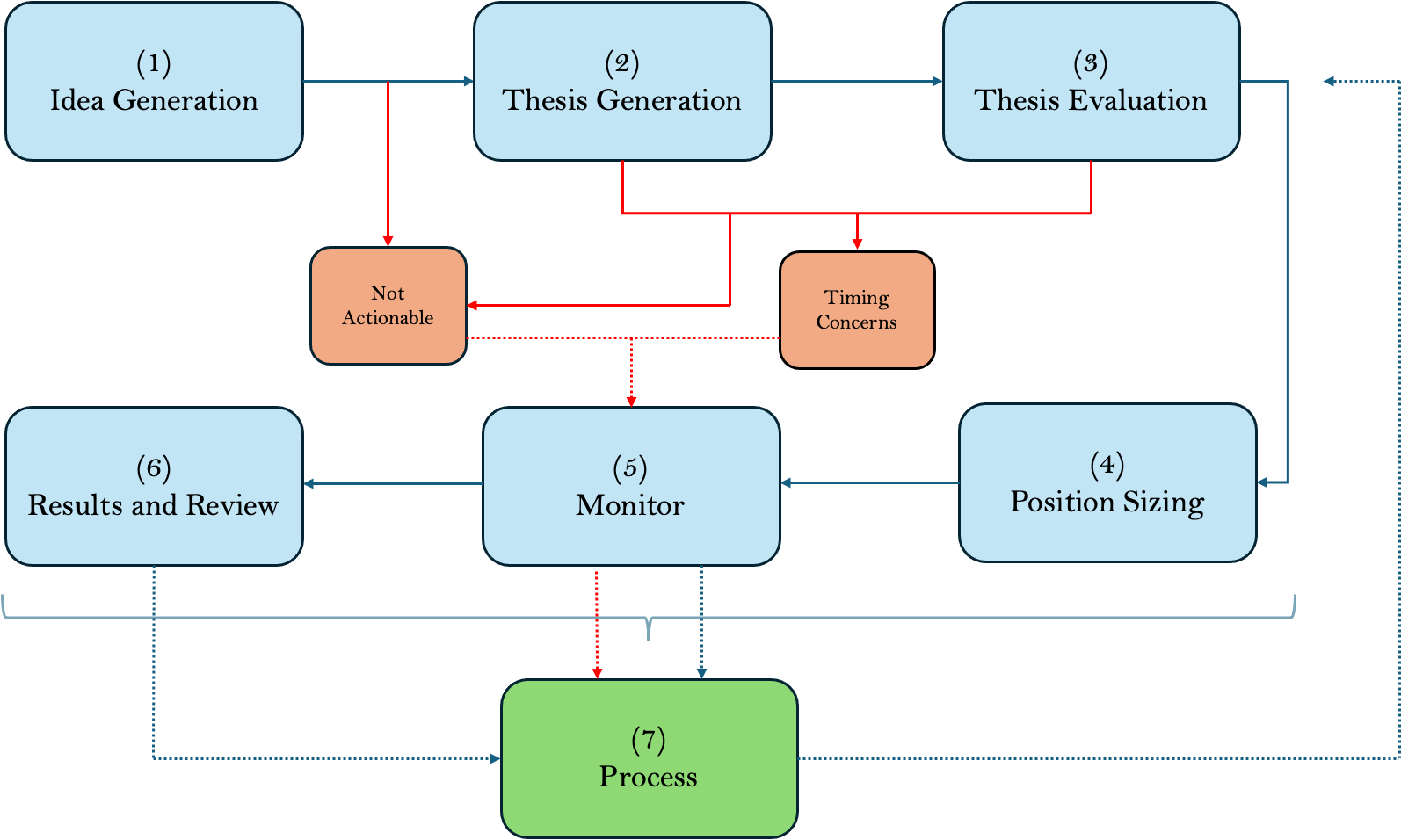

E. The Framework

Let us consider a system.

This objective is to minimise both errors of commission and errors of omission. It functions both as a filter funnel and an anti-fragile framework.

The natural filter of going from (1) to (4) stress tests the potential idea through multiple rounds of evaluation from various angles. The byproduct of the filter, however, is not all junk. Some will be monitored for either educational purposes or potentially being part of the future idea-generation pool. The results of these byproducts are monitored and evaluated for errors of omission.

The ongoing reflective process in (5) and the post-mortem evaluation in (6) seek to enhance the robustness of the process (7). The process encompasses stages (1) to (6), each stage with its trove of framework and guidelines.

Idea generation: Step 1 is to search out the pond that is small, neglected, and fertile for fishing. Companies in this pool are typically desperate to do what is ‘right’ due to ailing sentiments and have a low bar to do so (easy correction of past mistakes).

Thesis generation: Step 2 is to identify the key factors that make or break the thesis. What is the thesis dependent on? Invert: What may break the thesis? Is it difficult for the thesis to go wrong? Are there multiple ways to win? Establish the possibilities of the outcomes.

Thesis Evaluation: Step 3 is about diving deep into the probabilities of the possibilities. Do you have aligned management with the same interests as you? Any insider purchases, share buybacks, ‘positive’ language in earnings call? Is the management capable? Is the business easy to understand? How clear are you with the underlying business? What is the propensity of any of the factors to change? How will the identified key factors affect your thesis?

Position Sizing: The decision behind position sizing considers capital preservation and risk-reward. We will cover this below.

Monitor: I monitor the companies I invested in and those I almost invested in. Here, we attempt to catch errors of omission and errors of commission.

Results and review: A post-mortem evaluation of the investment (or the lack thereof). Are the results as expected in the thesis? How would I attribute the results to luck vs correct judgment? Was the position size optimal and what can be improved in the process? This is a tricky business as outcomes frequently mask the quality of the underlying process in the short run. However, in the longer term, the process determines results.

F. Investor’s bias & heuristics

You may be familiar with the 24 standard causes of Human Misjudgment by Charlie Munger. If you have not, I highly recommend reading it here. I will not reiterate all the points as that adds no value to you and me but I will highlight a few of mine that I have found invaluable.

He who is often reproved, yet stiffens his neck, will suddenly be broken beyond healing.

Proverbs 29:1

Pride

Investing in a new company is always exciting. After 80 hours of research, you have covered all grounds and are ready to rule the world. But just a month later you may find yourself nursing your wounds because you had blindspots.

Constantly maintaining a rationally reflective attitude allows us to improve upon our process by making rounds of mistakes and successes - especially the mistakes.

Always be teachable or you will stop learning.

Better is the end of a thing than its beginning,

and the patient in spirit is better than the proud in spirit.Ecclesiastes 7:8

Impatience

Impatience and impulse lead to blind spots. The fear of missing out leads to herding. A patient investor evaluates rationally rather than emotionally.

A patient investor treads cautiously rather than pridefully.

Attachment bias

When facts and views change, the position must change too. Do not be emotionally attached just because you have held it for long or you recently invested.

Being Market Jr.

Behaving in a way that resembles Mr. Market - being impulsive, fear of missing out, investing on hopes and dreams, dumping on doomsday scenarios, having little to no regard for fair value when transacting, allowing the price to lead your narrative, caring about what the broad market is doing, attempting to predict what the broad market does in the short-medium term, caring about macro, caring about short term movements, caring about what others think, distracted by the sea of noise, etc.

Underestimating the power of incentives

This will be covered in the next section.

G. Incentives

For where your treasure is, there your heart will be also.

Matthew 6:21

We are undoubtedly motivated by incentives. We are self-interested and this self-interest has gotten us pretty much nowhere collectiely. Our behaviours reflect our hearts and desires.

You can count on incentivized managers to maximise shareholder value and count on the rest to maximise their compensation. The former may choose to liquidate and wind down operations to unlock hidden value while the latter may embark on a value-destructive acquisition spree to expand its empire. We may have the same boat but different captains, leading to opposing destinations.

Dig deeper into the C-suite’s and the board’s incentives. How much skin in the game do they have?

And the Lord God commanded the man, “You are free to eat from any tree in the garden; but you must not eat from the tree of the knowledge of good and evil, for when you eat from it you will certainly die.

Genesis 2:16-17

Exceptions - where managers may sometimes, uncharacteristically, act in ways that oppose their incentives. Humanity rebelled against God because of pride. Managers can betray their incentives for their pride in a boardroom struggle. Do not underestimate supposedly intelligent individual’s ability to swiftly tear down what they have built.

H. N’th-order thinking

It is important to observe first-order thinking in the market. They are typically the birthplaces of inefficiencies. When a myopic narrative starts to take shape, you may find yourself a promising idea.

Second-order thinking is required for the construction of valid contrarian views. You are not trying to be different for the sake of it but to identify the gaps in thinking due to heuristics and biases in the market.

N’th-order thinking is required to stress-test your views and process over the longer term. Take the example of incentives above - it is important to understand the incentives and the exceptions that violate the rule.

I attempt to combat biases by demanding probabilistic thinking and clarity in the thesis.

The fair value of any company today should reflect the weighted average of the probabilities of possibilities; each event being a node that branches out to more possibilities. Anything can happen. A meteor can strike the vessel or the exploration miner can strike the largest reserve discovery ever. My job is to narrow the infinite range into a manageable set of probable scenarios with varying material outcomes for evaluation. If I am not able to, it belongs in the too-hard pile.

I will then evaluate the certainty and clarity of these events. How certain am I that this tree covers 80% of all material possibilities? Are there numerous moving parts that are hazy and uncertain? What happens if everything goes wrong? Am I trying to sound smart or am I trying to find the best opportunities?

Evaluate facts and observations systematically while leaving room for the unexpected.

I. Position Sizing

Give a portion to seven, or even to eight,

for you know not what disaster may happen on earth.Ecclesiastes 11:2

Wise position sizing bridges a good investment and a well-constructed portfolio. It carries the boldness of a thoroughly analysed investment idea and the humility of facing uncertainties.

Over time, I believe that the pursuit of capital preservation should be deferred from the individual stock to the portfolio management level. An idea with a 20% chance of 100% loss but an 80% chance of a 1000% gain should be part of the portfolio but sized accordingly. If capital preservation is considered prematurely at the stock level (to invest or not), one may commit the error of omission.

The decision is a function of considering the downside, the upside, and the respective probabilities. The optimal number of position in my portfolio stands at 7 - forcing me to select only the best ideas. There are more to this but let’s leave it for another day.

Part B. Review of mistakes and wins

A. Mistakes

The following are the blunders I made just this year.

Spirit Airlines (SAVE)

A thesis that revolved around Jetblue’s acquisition of Spirit Airlines. Facts, historical case statistics, expert opinions, and the progress of the court hearing pointed towards a favourable outcome for SAVE’s shareholders. But the judge had the final say and ruled otherwise.

SAVE’s fundamentals have since eroded and expected to file for bankruptcy soon. Such an outcome is not consumer-friendly, contrary to what the judge hoped for in blocking the deal.

The deal with seemingly more anti-trust concerns, Alaskan Airlines’ acquisition of Hawaiian Airlines, closed instead.

What I missed: SAVE’s operations deteriorated drastically. The magnitude of capital loss grew over time and even if the thesis remained attractive, it would have been wise to trim the position.

Yellow Corporation (YELLQ)

Going through Chapter 11 liquidation proceedings with assets expected to be materially larger than total liabilities. It was flung into bankruptcy unfairly by the worker union’s head and its business relations were permanently impaired. As a result, they were forced to file for bankruptcy.

There is a huge pension obligation claim against YELLQ that was already funded by the government during COVID. The expectations were that YELLQ should be off the hook since it was already funded. There should not be double-dipping. The judge ruled otherwise.

What I missed: There were too many moving parts - pension obligations, WARN Act claims, etc. Instead of having multiple ways of winning, we had many ways of losing.Alignment of interests was also insufficient here. Bondholders took a sizeable position in YELLQ’s equity reflecting their confidence in recovery. Management and shareholders are aligned. But all that matters is, once again, the judge’s decision.

Talis Biomedical Corp (TLIS)

NCAV substantially more than market capitalisation with a ‘typical’ shareholder litigation overhang.

What I missed: Management has no skin in the game and preferred to drag out the process to line up their own pockets instead. They filed for an expensive bankruptcy to deal with the litigation while paying themselves millions.Superdry PLC (SDRY)

The founder offered to privatise the company after years of deteriorating business fundamentals. CEO had more than 30% of the company and repeatedly voiced confidence in turning the business around.

What I missed: Retail businesses deteriorate mercilessly once out of fashion. Turnarounds are notoriously difficult to pull off, let alone turnarounds in retail. The toxic debt ramping up in the company should have sounded alarms. There was a low likelihood that the CEO could secure financing to privatise Superdry.

Sezzle (SEZL)

Low P/E payments company that was beaten down by the 20/21 technology bubble popping. It is highly cash flow generative and priced at a depressing 8-10x free cash flow with a strong balance sheet. Strong insider purchases and was listed on the Australian Stock Exchange. 70% of its business was based in the U.S.. The management decided to relist Sezzle on the US stock exchange instead.

What I missed: I sold after it was relisted. I was occupied with other positions and ignored Sezzle, which had a low bar considering its former valuation. It went on to more than 10x the price I sold at.

B. Wins

These wins come rarely but when they do, they contribute to the majority of the portfolio’s performance when sized appropriately.

They share the following characteristics and traits:

Starts completely depressed due to overhang - operational mistakes and capital allocation mistakes in the past. This led to the loss of shareholder confidence and a tighter credit environment. (GME, DXLG, TER.AX, GMS.LN, OPRT - they started off pricing at 1-3x P/nFCF).

Strong and stable underlying business that does not require much management involvement (TER.AX, GMS.LN)

Strong and stable free cash flow goes towards rapid deleveraging. (TER.AX, GMS.LN, OPRT)

Revert towards being accepted as a ‘normal’ functioning business by the market (GME, DXLG, TER.AX, GMS.LN, OPRT)

There are numerous ways to win and ‘difficult’ to lose. It takes a lot to derail the thesis. (TER.AX, GMS.LN, OPRT)

Huge margin of safety financially and operationally (GME, GMS.LN, TER.AX, OPRT)

Fundamentals are already clearly improving (TER.AX, GMS.LN, OPRT) or will certainly improve because of clear inevitable inflection (GME, DXLG).

Part C. Current portfolio

The portfolio currently consists of 6 positions with 80% allocated. I will briefly summarise each of its thesis and update it separately in a write-up in the future.

Oportun Financial: A financial institution that was suffering from years of mismanagement. OPRT attempted to cajole venture capital, acquired a digital bank, and doubled its operating expense by aggressively hiring unnecessarily. This did not accompany a proportional increase in revenue and asset yield, wiping out all of its earnings. This pushed OPRT to a dire credit situation operationally. It is undercovered and largely ignored by the market. OPRT is down 90% since the high of 2021.

An activist got involved last year and doubled its position this year.

Since 2Q22, the management has cut OPRT’s operating expenses from 22.6% to 13.8%, improved loan book credit quality, and stabilised loan book shrinkage. Even though OPRT is in a much better position today vs last year, it is down 33% YTD, reflecting shareholder fatigue and a lack of confidence in management.

OPRT has 2 toxic debts costing 16% for the Jan 25 tranche and 17% for its Sep 26 tranche. Since the beginning of the year, OPRT has been paying down its debt using its organic operating cash flow, leaving just $38M for its Jan 25 tranche and $109 for its Sep 26 tranche. OPRT averages $100M of operating cash flow a year. If they continue to control their operating expenses and maintain their credit quality, deleveraging should be even less of an issue.

OPRT is my largest position.

Gulf Marine Services: I have previously trimmed my position drastically at 20p or so accounting for how much it has re-rated. Its fundamentals have been catching up while price remained depressed by technical selling of its (formerly) largest shareholder Seafox. This created an opportunity for me to re-establish GMS as my second-largest position. It trades at 2.5x P/FCF and 4.5x EV/FCF while peers trade at 7-8x EV/FCF. Deleveraging itself will offer a 100% upside and rerating another 100%, giving us up to 400% in the next 2-5 years. This does not account for any possible further favourable tightening of the offshore industry.

Aviation PLC. AVAP is an aircraft leasing company listed in the UK and headquartered in Singapore. It is priced depressingly even though fundamentals have improved markedly since COVID. Its NAV has grown to 2.85 GBP a share while it trades at 1.66 GBP a share today. It has successfully sold its aircraft at book and extended its existing contracts at high rates.

Rusoro Mining. RML’s mines were illegally expropriated by the Venezuelan government on 14 March 2012. They were awarded more than $1.8B in compensation by the international tribunal court but did not receive any payment. In 2023, Venezuela’s ‘alter ego’, PDVSA, owns Citgo, a refinery owned by Venezuela situated in the states. Claimants proceeded with the sale of Citgo to fund the claims against Venezuela regarding the expropriation. RML claim priority sits behind around $5.5B of other claimants and debt holders. The highest bid so far is at $7.38B, making RML’s $1.7B-$1.8B claim whole before any transaction-related fees are incurred. It is not as straightforward as it seems - lower-priority claimants are filing lawsuits in hopes of getting a chunk of the pie while the bidding process is now uncertain and muddy. RML’s market capitalisation is currently USD 460M.

Montero Mining and Resources. MON.V’s claim against Tanzania follows that of Winshear Gold and Indiana Resources - both have achieved settlement and actual payment from the government of Tanzania. Winshear settled at 30c on the dollar claimed against Tanzania and received payment before the trials started. Indiana Resources settled at 80c after Tanzania’s final appeal failed. While Montero is priced at less than 30c on the dollar claimed.

ContextLogic. A shell company trading at below net cash with huge tax assets ripe for monetisation.

Conclusion

Cast your bread upon the waters,

for you will find it after many days.Ecclesiastes 11:1

The last four years of investing have been such great joy and growth. God has blessed me with supernormal returns since inception while teaching me amazing lessons through my mistakes. The pursuit has taught me patience and humility. I have learnt to recognise and acknowledge God’s hands in all that I do and am immensely grateful to Him.

If you have read through all of the above, I am impressed.

May the Lord bless you.

Joshua

Disclaimer:

The information contained herein reflects the opinions and projections of Joshua Zeng, as of the date of publication, which is subject to change without notice at any time after the date of issue. All information provided is for informational purposes only and should not be deemed as investment advice or recommendation to purchase or sell any specific security/asset. While the information presented herein is believed to be reliable, no representation or warranty is made concerning the accuracy of any data presented. Positions reflected in this presentation do not represent all the positions held, purchased, or sold, and in the aggregate, the information may represent a small percentage of activity. The information presented is intended for Joshua Zeng to illustrate his own thoughts for his own learning purposes only. All funds managed under Joshua Zeng wholly belong to him and him alone.